Money Market Fund – Your Soft Life Hack!

We have heard a lot about Money Market Funds or in short MMFs and with good reason, MMFs have been the go-to asset for anyone who’s ever thought, ‘I just want my money to work for me while I chill’. By now you can almost be guaranteed it’s the one financial asset every Kenyan knows. But before we get carried away, MMFs are a part of a squad called Unit Trusts. In a previous post, Unit Trusts in Kenya, I wrote about unit trusts. Just to recap, unit trusts are collective schemes where fund managers pool investors’ money – like a financial chama, to put in a diversified portfolio to earn return remitted to investors at the end of every month as interest earned – this is now passive income! Investors can then choose to reinvest the interest or withdraw; I recommend reinvesting. One unit goes for one shilling; a 1:1 proportion, no forex drama here.

Disclaimer: Investing in MMFs carries risks, and past performance (empirical data) is not indicative of future results. Make sure to do your own due diligence and if you prefer can consult with a financial advisor to guide you before making any investment decisions. Be sure to confirm you are dealing with a legitimate financial advisor and don’t share your personal details; security details included.

Now that we have an idea of what unit trusts are, which children belong to the Unit Trust family? We have Equity fund, Fixed income fund, Wealth fund, Balanced fund, Bond fund among others. Each of these track performances of specific assets which bear different risk and return levels. For example, an equity fund invests in equities, fixed income fund in fixed income assets e.g., certificate of deposits and government securities. Unit trusts can also be denominated in both Kenya shillings and USD to leverage on the currency conversion especially for the dollar ballers, you can also flex with a USD MMF.

Why are Kenyans obsessed with MMFs?

In the past 2 or three years, there has been a huge prevalence albeit a lingering reluctance in general exploration of saving and investing. Money market funds are provided by fund managers who are regulated by the Capital Markets Authority (CMA) – this is like the watchman or spy to protect investors from malpractices and prohibit illegal trading. It’s vital to know every asset you consider must be from a regulated entity; don’t just give your money to anyone with flashy logo or social media page – stay vigilant! You can confirm your fund manager is legit by visiting the CMA website and checking the list of licensees. Let me save you the hustle, here’s a direct ticket to the list: CMA List of Licensees.

The team that makes the dream work

There are key features to understand about Money Market Funds. The first one of course being a fund manager regulated by CMA – ensures investors’ money works for them like it owes them. See a list for the other features:

- Trustee – uses investors’ money for their good.

- Custodian – safeguards investors’ money.

This is my preferred analogy of these two features: Imagine a library, a librarian mans the books so is in custody of these books (books = money). When you borrow a book, you are entrusted with the book that you’ll use it and bring back in good condition. In this case, the librarian becomes the custodian and you the trustee. Fun fact: A fund manager is neither the trustee nor custodian. They must be independent parties.

How much do you need to start and maintain your MMF account?

- Minimum investment – this varies across funds but most range between KES 100 – KES 5,000. This is the initial amount you deposit when you open an account.

- Minimum top-up – it varies across funds. There’s no ceiling to how much you can deposit but there’s a floor which ranges between KES 100 – KES 1,000.

An investor can deposit as often as they can. There’s no requirement to how often you should deposit in your account. An investor can also withdraw from their account at any time either to your MPESA or bank account, confirm with your fund manager.

Even Soft Life comes with terms and conditions

A fund manager’s role is to manage portfolio and use their expertise to develop investment strategies i.e., how investors’ pooled money will be invested in different asset classes to leverage on favourable returns. This work comes with a small fee imposed on investors but deducted at source. These fees are already factored in in the overall return an investor receives. Other charges deducted from the interest earned is the withholding tax, the taxman must also eat.

- Management fee – Usually 2% of gross interest earned. For example, an investor receives 16% gross interest. An investor’s net interest will be 14%. It may not be seen in statement as these are calculations done in the back end but doesn’t limit an investor from enquiring what percentage is the management fee.

- Withholding tax (WHT) – Money Market Funds are subject to 15% WHT deducted at source i.e., from the interest earned. For example, in a month an investor earns KES 6000 in interest. The net interest hitting their account will be KES 5,100.

What about exits?

Not to be scared, with Money Market Funds the exit strategy is simple. No exit fees or penalties! If you want to dip, just contact your fund manager to close your account, and your money will be deposited to your registered bank account.

How do investors make money from MMFs?

An investor deposits money as often as they prefer. At the end of the month, interest is credited to their account with a breakdown visible at all times on their fund managers portal. An investor can choose to withdraw the interest or reinvest it to continue earning interest on interest a concept called compounding interest. It is only reasonable to withdraw your interest if it’s enough to fund your real financial goal. An investor gives a one-time instruction to the fund manager to deposit the interest in their account monthly.

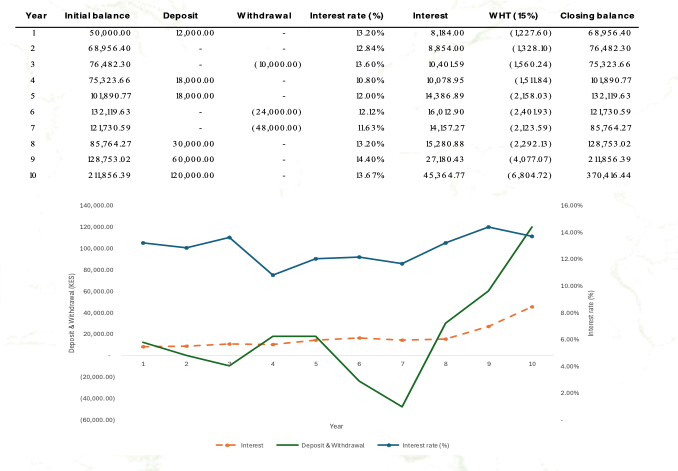

Below is a sample of an investor’s MMF deposits, withdrawals, taxation and visual representation of MMF performance over a period of 10 years

Time to act like your wallet has a strategy

MMFs are the most stress-free and simplest asset to have in your portfolio. Review your spending and budget for a saving or investment in a Money Market Fund today – your future self will already be drafting a vote of thanks probably while cruising in a yacht somewhere.

Need a guiding hand with MMFs and more? Contact us to help you develop financial wisdom and confidence with handling your finances.